François Jonquet

François Jonquet Carlos Alba

Carlos Alba Sergio Castañeira

Sergio Castañeira Tommaso Protti

Tommaso Protti Horst Pannwitz

Horst PannwitzTNT Express und FedEx Corp vs. PostNL und Deutsche Post – kommentierter KW 52 Peer Group Watch Post

30.12.2023, 6440 Zeichen

In der Wochensicht ist vorne:

TNT Express 1,59% vor

FedEx Corp 1,45%,

Nippon Express 0%,

Österreichische Post -0,15%,

United Parcel Service -0,2%,

Deutsche Post -0,56% und

PostNL -1,65%.

In der Monatssicht ist vorne:

TNT Express 8,45% vor

Deutsche Post 6,95%

,

United Parcel Service 4,85%

,

Nippon Express 3,96%

,

Österreichische Post 2,67%

,

FedEx Corp -1,05%

und

PostNL -3,38%

.

Weitere Highlights: PostNL ist nun 3 Tage im Minus (1,65% Verlust von 1,45 auf 1,43).

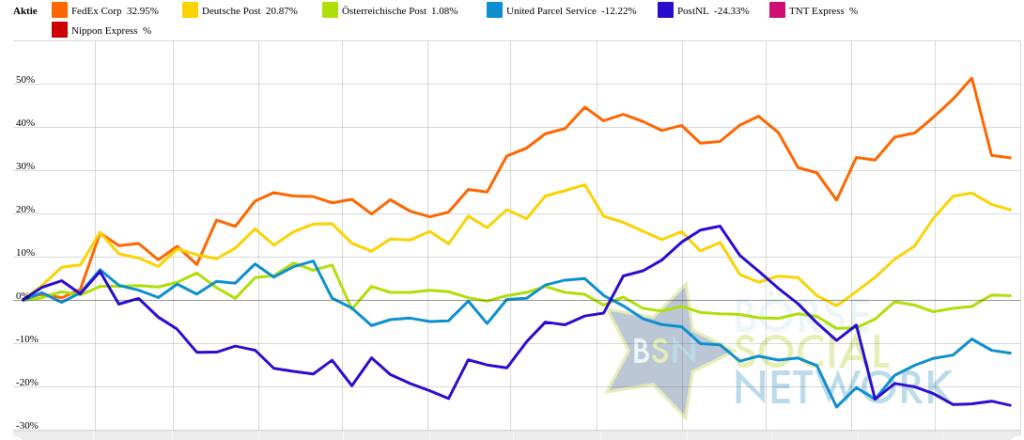

Year-to-date lag per letztem Schlusskurs

FedEx Corp 44,88% (Vorjahr: -33,01 Prozent) im Plus. Dahinter

Deutsche Post 27,06% (Vorjahr: -37,78 Prozent) und

Österreichische Post 11,22% (Vorjahr: -22,22 Prozent).

PostNL -15,93% (Vorjahr: -56,11 Prozent) im Minus. Dahinter

United Parcel Service -9,78% (Vorjahr: -18,73 Prozent) und

Nippon Express -1,87% (Vorjahr: 3,88 Prozent).

Am weitesten über dem MA200:

Deutsche Post 6%,

FedEx Corp 2,34% und

Österreichische Post 1,18%.

Am deutlichsten unter dem MA 200:

TNT Express -100%,

PostNL -16,7% und

Nippon Express -11,35%.

Hier der aktuelle ausserbörsliche Blick.

Vergleicht man die

aktuellen Indikationen bei L&S mit dem letzten Schlusskurs, so lag um 8:38 Uhr die

TNT Express-Aktie am besten: 11,41% Plus. Dahinter

FedEx Corp mit +1,55% ,

Nippon Express mit +0,95% ,

United Parcel Service mit +0,93% ,

Deutsche Post mit +0,36% ,

PostNL mit +0,1% und

Österreichische Post mit -0,23% .

Die Durchschnittsperformance ytd der BSN-Group Post ist 7,94% und reiht sich damit auf Platz 13 ein:

1. Computer, Software & Internet : 39,12%

Show latest Report (30.12.2023)

2. Bau & Baustoffe: 37,61%

Show latest Report (30.12.2023)

3. Big Greeks: 27,23%

Show latest Report (30.12.2023)

4. PCB (Printed Circuit Board Producer & Clients): 23,13%

Show latest Report (30.12.2023)

5. Börseneulinge 2019: 21,6%

Show latest Report (30.12.2023)

6. IT, Elektronik, 3D: 19,43%

Show latest Report (30.12.2023)

7. Crane: 18,02%

Show latest Report (30.12.2023)

8. Versicherer: 16,37%

Show latest Report (23.12.2023)

9. Deutsche Nebenwerte: 15,11%

Show latest Report (30.12.2023)

10. Luftfahrt & Reise: 12,98%

Show latest Report (30.12.2023)

11. MSCI World Biggest 10: 11,17%

Show latest Report (30.12.2023)

12. Immobilien: 11,09%

Show latest Report (30.12.2023)

13. Post: 7,94%

Show latest Report (23.12.2023)

14. Global Innovation 1000: 6,48%

Show latest Report (30.12.2023)

15. Runplugged Running Stocks: 6,41%

16. Stahl: 6,17%

Show latest Report (23.12.2023)

17. Banken: 5,79%

Show latest Report (30.12.2023)

18. Auto, Motor und Zulieferer: 5,54%

Show latest Report (30.12.2023)

19. Telekom: 5,01%

Show latest Report (23.12.2023)

20. Konsumgüter: 4,9%

Show latest Report (30.12.2023)

21. Zykliker Österreich: 2,09%

Show latest Report (23.12.2023)

22. Energie: 1,29%

Show latest Report (30.12.2023)

23. Media: -0,34%

Show latest Report (30.12.2023)

24. Sport: -3,03%

Show latest Report (23.12.2023)

25. Ölindustrie: -3,63%

Show latest Report (30.12.2023)

26. Pharma, Chemie, Biotech, Arznei & Gesundheit: -6,21%

Show latest Report (30.12.2023)

27. Rohstoffaktien: -8,75%

Show latest Report (23.12.2023)

28. Gaming: -11,26%

Show latest Report (30.12.2023)

29. Aluminium: -11,53%

30. Solar: -12,2%

Show latest Report (23.12.2023)

31. OÖ10 Members: -15,77%

Show latest Report (30.12.2023)

32. Licht und Beleuchtung: -16,21%

Show latest Report (30.12.2023)

Social Trading Kommentare

|

Deutsche Post AG is fairly valued and with expected growth rates of 6% to 8% a hold. The historic average P/E is around 14 and at today price of 44,70€ exactly at this valuation. While the dividend of 4,14% is still attractive and with a payout ratio pf 26% of operating cashflow reasonable safe. Analysts excepct a 1% operating cashflow growth in 2024 and 6% in 2025. Return on total capital (ROTC) stands for Deutsche Post at around 8% to 9% on a 5 year average. Operating earnings and free cash flow grew on average 6% per year in the last two decades. When you consider analysts expectations, ROTC, average growth numbers the PE of 14 looks fairly valued. Remember, a PE of 14 equals to a 7,1% earnings yield. With that numbers Deutsche Post is a solid hold. I would expect the stock to return 11% including dividends for the comming years. This is in my humble opinion to high to sell and to less to buy. At a price price of under 39€ I would reconsider this title to be added to the High Quality Dividend Growth portfolio. |

|

|

Deutsche Post AG is fairly valued and with expected growth rates of 6% to 8% a hold. The historic average P/E is around 14 and at today price of 44,70€ exactly at this valuation. While the dividend of 4,14% is still attractive and with a payout ratio pf 26% of operating cashflow reasonable safe. Analysts excepct a 1% operating cashflow growth in 2024 and 6% in 2025. Return on total capital (ROTC) stands for Deutsche Post at around 8% to 9% on a 5 year average. Operating earnings and free cash flow grew on average 6% per year in the last two decades. When you consider analysts expectations, ROTC, average growth numbers the PE of 14 looks fairly valued. Remember, a PE of 14 equals to a 7,1% earnings yield. With that numbers Deutsche Post is a solid hold. I would expect the stock to return 11% including dividends for the comming years. This is in my humble opinion to high to sell and to less to buy. At a price price of under 39€ I would reconsider this title to be added to the High Quality Dividend Growth portfolio. |

SportWoche Podcast #106: Persönliches Fail-Fazit VCM und Staatsmeisterin Carola Bendl-Tschiedel über Rekordlerin Julia Mayer

Bildnachweis

1.

BSN Group Post Performancevergleich YTD, Stand: 30.12.2023

2.

Briefkasten, Brief, aufgeben, Post, Mailbox, schreiben, http://www.shutterstock.com/de/pic-156790661/stock-photo-close-up-of-woman-s-hand-holding-envelope-and-inserting-in-mailbox.html

>> Öffnen auf photaq.com

Aktien auf dem Radar:Immofinanz, Polytec Group, Marinomed Biotech, Flughafen Wien, Warimpex, Lenzing, AT&S, Strabag, Uniqa, Wienerberger, Pierer Mobility, ATX, ATX TR, VIG, Andritz, Erste Group, Semperit, Cleen Energy, Österreichische Post, Stadlauer Malzfabrik AG, Addiko Bank, Oberbank AG Stamm, Agrana, Amag, CA Immo, EVN, Kapsch TrafficCom, OMV, Telekom Austria, Siemens Energy, Intel.

Random Partner

BNP Paribas

BNP Paribas ist eine führende europäische Bank mit internationaler Reichweite. Sie ist mit mehr als 190.000 Mitarbeitern in 74 Ländern vertreten, davon über 146.000 in Europa. BNP Paribas ist in vielen Bereichen Marktführer oder besetzt Schlüsselpositionen am Markt und gehört weltweit zu den kapitalstärksten Banken.

>> Besuchen Sie 68 weitere Partner auf boerse-social.com/partner

Autor

Christian Drastil

Christian Drastilhttp://www.boerse-social.com , http://photaq.com bzw. https://www.wikifolio.com/de/at/p/smeilinho

Useletter

Die Useletter "Morning Xpresso" und "Evening Xtrakt" heben sich deutlich von den gängigen Newslettern ab.

Beispiele ansehen bzw. kostenfrei anmelden. Wichtige Börse-Infos garantiert.

Newsletter abonnieren

Runplugged

Infos über neue Financial Literacy Audio Files für die Runplugged App

(kostenfrei downloaden über http://runplugged.com/spreadit)

per Newsletter erhalten

| AT0000A39UT1 | |

| AT0000A2U2W8 | |

| AT0000A2K9L8 |

- Wiener Börse Party 2024 in the Making, 27. April ...

- Wiener Börse Party 2024 in the Making, 26. April ...

- 21st Austria weekly - Palfinger, Polytec (26/04/2...

- 21st Austria weekly - Strabag, S Immo (25/04/2024)

- 21st Austria weekly - Amag (24/04/2024)

- 21st Austria weekly - Erste Group, Strabag, Verbu...

Featured Partner Video

D&D Research Rendezvous #6: Gunter Deuber nach der RBI-Zürs-Konferenz zu ATX, Stimmung, Geopolitik, Asset-Klassen, Oddo-BHF

Gunter Deuber, Head of Raiffeisen Research, trifft sich mit Podcast-Host Christian Drastil jeden Monat zum "D&D Research Rendezvous". In Folge 6 geht es um ein Zwischenfazit nach 15 Woc...

Books josefchladek.com

Index Naturae

2023

Skinnerboox

Liebe in Saint Germain des Pres

1956

Rowohlt

Nacht und Nebel

2023

Safelight

Federico Renzaglia

Federico Renzaglia Futures

Futures

MichaelB

zu DPW (29.12.)

Deutsche Post AG is fairly valued and with expected growth rates of 6% to 8% a hold. The historic average P/E is around 14 and at today price of 44,70€ exactly at this valuation. While the dividend of 4,14% is still attractive and with a payout ratio pf 26% of operating cashflow reasonable safe. Analysts excepct a 1% operating cashflow growth in 2024 and 6% in 2025. Return on total capital (ROTC) stands for Deutsche Post at around 8% to 9% on a 5 year average. Operating earnings and free cash flow grew on average 6% per year in the last two decades. When you consider analysts expectations, ROTC, average growth numbers the PE of 14 looks fairly valued. Remember, a PE of 14 equals to a 7,1% earnings yield. With that numbers Deutsche Post is a solid hold. I would expect the stock to return 11% including dividends for the comming years. This is in my humble opinion to high to sell and to less to buy. At a price price of under 39€ I would reconsider this title to be added to the High Quality Dividend Growth portfolio.

MichaelB

zu DPW (29.12.)

Deutsche Post AG is fairly valued and with expected growth rates of 6% to 8% a hold. The historic average P/E is around 14 and at today price of 44,70€ exactly at this valuation. While the dividend of 4,14% is still attractive and with a payout ratio pf 26% of operating cashflow reasonable safe. Analysts excepct a 1% operating cashflow growth in 2024 and 6% in 2025. Return on total capital (ROTC) stands for Deutsche Post at around 8% to 9% on a 5 year average. Operating earnings and free cash flow grew on average 6% per year in the last two decades. When you consider analysts expectations, ROTC, average growth numbers the PE of 14 looks fairly valued. Remember, a PE of 14 equals to a 7,1% earnings yield. With that numbers Deutsche Post is a solid hold. I would expect the stock to return 11% including dividends for the comming years. This is in my humble opinion to high to sell and to less to buy. At a price price of under 39€ I would reconsider this title to be added to the High Quality Dividend Growth portfolio.