Slowing growth â the dilemma of the ECB (Martin Ertl)

2 weitere Bilder(mit historischen Bildtexten)

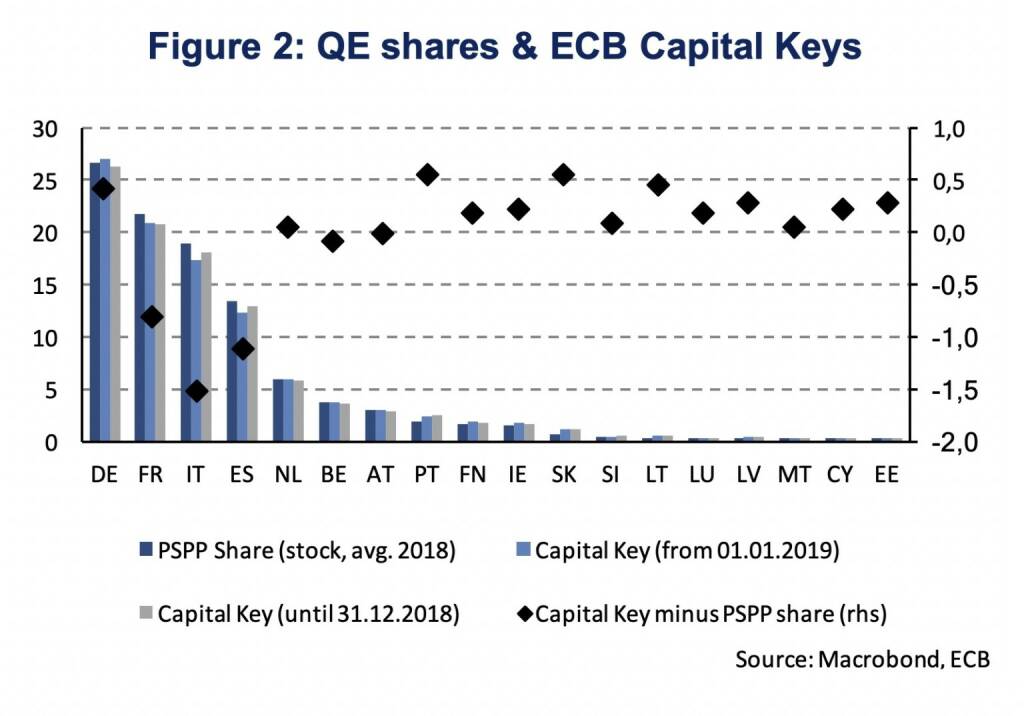

QE shares & ECB Capital Keys

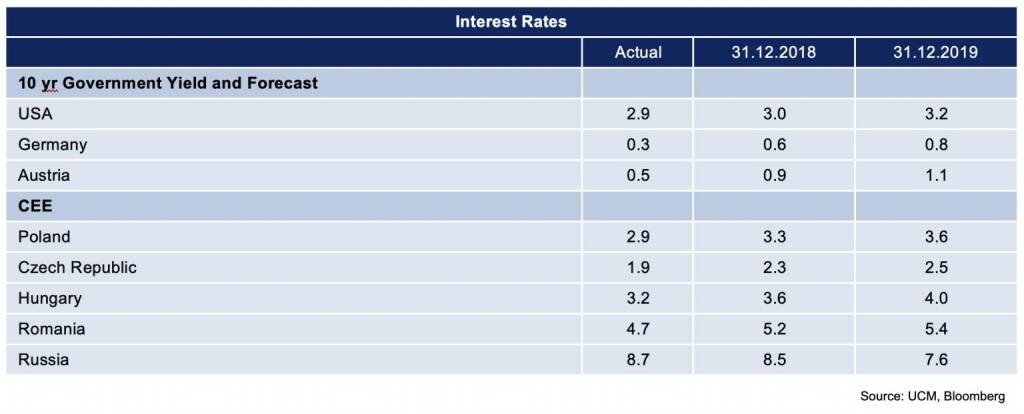

Interest Rates

Dimitri Bogachuk

Dimitri Bogachuk Olga Ignatovich

Olga Ignatovich Fabrizio Strada

Fabrizio Strada Daido Moriyama

Daido Moriyama17.12.2018, 6930 Zeichen

- Exit from QE has been confirmed, reinvestment of accumulated stock continues to provide accommodative monetary conditions.

- The December macro projections include downward revisions in GDP growth and inflation.

- Redemptions will be reinvested past the first increase in key interest rates. New ECB capital keys requires portfolio reallocation.

In the meeting of the governing council (GC) last Thursday, the ECB confirmed its exit from ultra-loose monetary policy or quantitative easing (QE). Net asset purchases under the asset purchase program (APP) will end by December. The accumulated stock of assets will, however, be reinvested, in full, for an extended period of time and past the date when the GC starts raising key interest rates. This was not unexpected as the US Federal Reserve has only started to reduce its balance sheet in October 2017, which was almost two years after the first interest rate hike in December 2015. Hence, even after the ECB initiates an interest rate hiking cycle, earliest in autumn 2019, the stock of accumulated assets will provide an ample degree of monetary accommodation. This is also known the stock effect.

The Euro Area business cycle has recently shown signs of a slowdown after a period of solid economic expansion. In Q3 2018, real GDP increased by meagre 0.2 % (q/q) The expenditure details revealed slow growth in household consumption (+0.1 %) and fixed investment (+0.2 %) and a quarterly decline in exports ( -0.1 %). Risk surrounding the Euro Area growth outlook can still be assessed as broadly balanced, according to the GC. However, President Draghi noted that “the balance of risks is moving to the downside owing to the persistence of uncertainties related to geopolitical factors, vulnerabilities in emerging markets and financial market volatility”. The December staff macroeconomic projections were released last week. Projections for GDP growth and inflation were revised downward compared to the September forecast. Real GDP is expected to grow by 1.9 %, 1.7 %, 1.7 % and 1.5 % between 2018 and 2021 (September: 2.0 %, 1.8 % and 1.7 % between 2018-2020). On a quarterly basis, the ECB expects GDP to rise by 0.4 % in Q4 2018 and 0.5 %, 0.5 %, 0.5 % and 0.4 % during Q1 to Q4 2019. Hence, the projection implies a rebound in quarterly growth momentum after a temporary slowdown during the second half of 2018.

HICP inflation is projected at 1.8 %, 1.6 %, 1.7 % and 1.8 % (September: 1.7 %, 1.7 % and 1.7 % in 2018-20). Core inflation (excluding energy and food prices) is expected to increase gradually by 1.0 %, 1.4 %, 1.6 % and 1.8 % (2018-21), while in September the ECB had projected core inflation of 1.1 %, 1.5 % and 1.8 % (2018-20). Hence, it is anticipated that it will take one more year until the inflation rate converges towards the central bank’s target below but close to 2 % (Figure 1).

Besides the more explicit forward guidance on reinvestment provided by the GC’s statement, the ECB has published a note on the technical parameters for reinvestment to provide further details. First, the accumulated stock of assets will be maintained under each constituent program. The composition of the asset purchase program, which consists of a public-sector purchase program (PSPP), an asset-backed securities purchase program (ABSPP), a covered bond purchase program (CBPP3) and a corporate sector purchase program (CSPP), will not change. Second, within the public-sector purchase program (PSPP) the allocation will continue to be guided by the national central banks’ subscription to the ECB capital key. This holds on a stock basis, such that the country shares of accumulated assets under the PSPP should correspond to the capital keys, adjusted for country participation in the PSPP.

Capital keys, however, are not fixed as they reflect a country’s share in the total population and gross domestic product of the EU, with equal weighting. New capital keys will become effective from the 1st January of 2019 onwards. Germany will face the largest percentage-point increase in its capital key (18 % to 18.4 %) while Spain (8.8 % to 8.3 %) and Italy (12.3 % to 11.8 %) will face the largest declines. In order to compare capital keys to the respective country shares in the PSPP, they need to be adjusted for Euro-Area membership and exclude Greece which has no participation in the PSPP. Figure 2 shows PSPP shares, adjusted capital keys on the left axis and the respective percentage point difference between the capital key and the PSPP share on the right axis. It can be seen that Italy (-1.5 %-age points), Spain (-1.1 %-age points) and France (-0.8 %-age points) face the largest negative difference between the PSPP share and the country’s respective capital key. Portugal, Slovakia (0.6 %-age points each) and Germany (0.4 %-age points) show the largest positive difference. Countries with a positive (negative) difference need to have a larger (smaller) allocation from reinvestment to bring the PSPP share in line with the capital key. As the capital key is partly determined by relative GDP, countries with lower GDP growth will also face a fall in demand from the PSPP.

The alignment of PSPP shares to capital keys will be gradual and done by reinvestments of the ECB rather than national central banks. The guidelines state that “redemptions will be reinvested in the jurisdiction in which principal repayments are made, but the portfolio allocation across jurisdiction will continues to be adjusted with a view to bringing the share of the PSPP portfolio into closer alignment with respective national central banks’ subscriptions to the ECB capital key.” From April 2016 onwards 10 % of monthly PSPP purchases (excluding supranational bonds) have been conducted by the ECB (8 % before April 2016) [1]. Redemption from these assets, which were accumulated via the risk-shared part of the PSPP, can now be reinvested to align PSPP shares to capital keys. The alignment will be gradual.

Despite the weaker growth outlook, QE ends (as was widely expected) and no new/additional monetary stimulus is yet provided. The new growth outlook hinges on a gradual rebound in quarterly growth momentum over the next months, while, for example, our own nowcast model keeps indicating a milder GDP growth rate until year-end (0.3 % q/q). The key ECB interest rates are expected to remain at their present levels at least through the summer 2019. The ECB stated more explicitly that an ample degree of monetary stimulus remains in place through reinvestment of maturing securities past the date when an interest rate hiking cycle starts. Future reinvestment from redemptions will gradually align PSPP shares to capital keys.

[1] Public sector purchase programme (PSPP)- Questions & Answers (https://www.ecb.europa.eu/mopo/implement/omt/html/pspp-q...

Authors

Martin Ertl Franz Xaver Zobl

Chief Economist Economist

UNIQA Capital Markets GmbH UNIQA Capital Markets GmbH

Börsepeople im Podcast S25/01: Christian Drastil (Plan CD)

Bildnachweis

1.

ECB staff inflation forecast

2.

QE shares & ECB Capital Keys

3.

Interest Rates

Aktien auf dem Radar:Frequentis, Agrana, Bajaj Mobility AG, EuroTeleSites AG, Amag, UBM, FACC, OMV, Verbund, Porr, Rosgix, EVN, AT&S, Rosenbauer, voestalpine, Wienerberger, Wolford, Wolftank-Adisa, BKS Bank Stamm, Oberbank AG Stamm, CPI Europe AG, Österreichische Post, Semperit, Telekom Austria, RHI Magnesita, DAX, Siemens, HeidelbergCement, MTU Aero Engines, Henkel, Fresenius Medical Care.

Random Partner

Freisinger

FREISINGER enterprises setzt auf Old-Economy im Bereich von technischen und industriellen Gütern. Persönlicher Kontakt mit einer guten Mischung aus E-Commerce ergeben eine optimale Vertriebsstruktur für technische Gase, Zubehör und Dienstleistungen.

>> Besuchen Sie 55 weitere Partner auf boerse-social.com/partner

Latest Blogs

» Börse People startet in die Jubiläums-Staffel 25 – zwischen Verlagspleit...

» Österreich-Depots: Mai Verfallstag (Depot Kommentar)

» Börsegeschichte 15.5.: EuroTeleSites, OMV (Börse Geschichte) (BörseGesch...

» Nachlese: Lina Mosentseva; Rheinmetall Love Trade? (audio cd.at)

» PIR-News: Strabag, Research zu RBI, wienerberger, Polytec, Semperit (Chr...

» Wiener Börse Party #1156: Mai-Verfallstag mit zunächst fallendem ATX, Ve...

» Wiener Börse zu Mittag leichter: Verbund, Frequentis und Semperit gesucht

» ATX-Trends: wienerberger, Flughafen Wien, Austriacard

» Österreich-Depots: Feiertags-Bilanz (Depot Kommentar)

Useletter

Die Useletter "Morning Xpresso" und "Evening Xtrakt" heben sich deutlich von den gängigen Newslettern ab.

Beispiele ansehen bzw. kostenfrei anmelden. Wichtige Börse-Infos garantiert.

Newsletter abonnieren

Runplugged

Infos über neue Financial Literacy Audio Files für die Runplugged App

(kostenfrei downloaden über http://runplugged.com/spreadit)

per Newsletter erhalten

- 21st Austria weekly - Strabag, Marinomed (11/05/2...

- Börse People startet in die Jubiläums-Staffel 25 ...

- 21st Austria weekly - Week 20 was finally an unch...

- Polytec Group und Mayr-Melnhof vs. Wienerberger u...

- Zurich Insurance und Allianz vs. Münchener Rück u...

- Orange und Telekom Austria vs. Vodafone und Tele ...

Featured Partner Video

Wiener Börse Party #1152: ATX dank RBI stärker, nun vor dem Euro-Stoxx-50 und wir machen ein Projekt mit Handball West Wien (Capitals)

Die Wiener Börse Party ist ein Podcastprojekt für Audio-CD.at von Christian Drastil Comm.. Unter dem Motto „Market & Me“ berichtet Christian Drastil über das Tagesgeschehen an der Wiener Börse. Inh...

Books josefchladek.com

Photographies Modernes Présentées par Pierre Bost

1927

Librairie des arts Décoratifs

Oculus

2018

Galerist & Galerie Filles du Calvaire

Polar Night

2019/2021

Trespasser

Anton Bruehl

Anton Bruehl Machiel Botman

Machiel Botman