Does the US economy need a mid-cycle adjustment? (Martin Ertl)

4 weitere Bilder(mit historischen Bildtexten)

US Labor Market (non-farm payrolls)

Inflation & Inflation Expectations

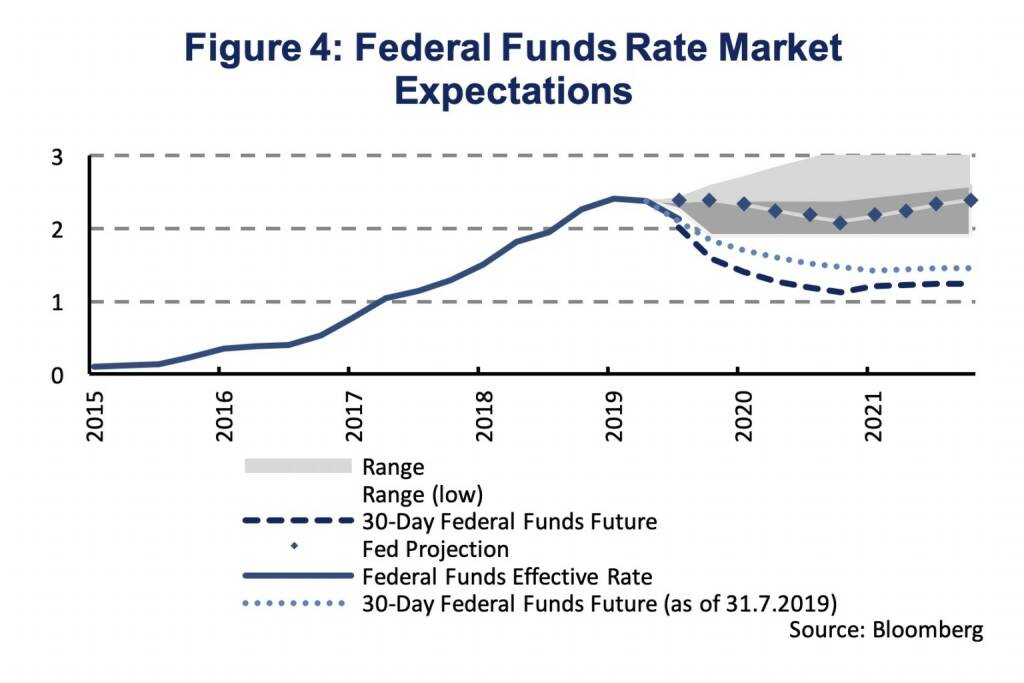

Federal Funds Rate Market Expectations

Interest Rates

Yusuf Sevinçli

Yusuf Sevinçli Ola Rindal

Ola Rindal Yusuf Sevinçli

Yusuf Sevinçli Joan van der Keuken

Joan van der Keuken Keizo Kitajima

Keizo Kitajima06.08.2019, 7363 Zeichen

- The US business cycle remains healthy, despite being the longest in history.

- Personal consumption drives the expansion, supported by a strong labor market.

- Fed lowered interest rate to 2.25 %, in light of trade related uncertainty and downside risks to the outlook.

- There is no clear-cut monetary policy case for the Fed’s mid-cycle adjustment, which remains ambiguous also within the FOMC.

The US economy continues its longest expansion since the end of WW II, exceeding the Great Moderation (03/1991-02/2001) by two months. The Bureau of Economic Analysis (BEA) has recently released its preliminary estimate of gross domestic product (GDP) for the second quarter of 2019 (Q2 19) at 2.1 % (seasonally adjusted at annual rates). With GDP growth at 3.1 % in Q1 2019, the US economy has expanded more rapidly during the first half of the year (2.6 %) than it did in 2018 (2.5 %, quarterly average). Thus, even though, growth has moderated somewhat in Q2 19, overall, the US economy is expanding at a solid rate.

Private consumption has been the main driver of GDP growth during the second quarter, contributing 2.85 %-age points (Figure 1). Also, government consumption, mainly federal nondefense expenditures, added to GDP growth (0.85 %-age points). Other factors subtracted from growth. Private investment declined and so did net exports. The decline in fixed investment, however, is less severe than it might seem, as changes in inventories led the decline (-0.86 %-age points). Net exports subtracted 0.65 %-age points from GDP growth with exports declining while imports stagnating.

The economy is supported by a strong labor market at full-employment and solid wage growth. In July, only 3.7 % of the US labor force was without a job and employment is further expanding. The Bureau of Labor Statistics reported that 164 thousand nonfarm jobs were created in July which is below, but close to, the benchmark of 200 thousand (Figure 2). Notable employment gains were reported in some service industries (professional and technical services, health care, social assistance and financial services) while employment in the manufacturing sector has not changed materially. In 2018 employment gains had averaged 223 thousand per month. In contrast, wage growth has not slowed down. Average hourly earnings increased by 3.2 % in July (y/y) which is in line with the average over the past 6 months. As long as the picture of low unemployment, steady job creation and solid wage gains prolongs, it is fair to assume that private consumption will further support the US expansion.

Based on already available business cycle indicators for the third quarter of 2019, the US economy is expected to grow between 1.6 (NY Fed) and 1.9 % (Atlanta Fed) in Q3. Similar to the previous quarter, consumer spending is expected to be the main growth driver. If a similar pace can be maintained in Q4, the US economy would grow by 2.3 % in 2019. The Federal Reserve Board members and Federal Reserve Bank presidents have projected GDP growth at 2.1 % for the year 2019, based on their assessment in June (median of Fed Economic Projections). Thus, it might well be that US growth tops previous estimates.

Given the state of the US economy it might, thus, come as a surprise that the Federal Reserve Bank (Fed) has decided to ease monetary conditions. Last week, the Federal Open Market Committee (FOMC) decreased the federal funds rate by 25 basis points (bp) to range between 2.0 and 2.25 %. It has been the first interest rate cut since December 2008 when the Fed lowered the federal funds rate to range between 0 and 0.25 %. Moreover, it marks the end of an interest rate hiking cycle which started in December 2015 and ended three years later in December last year.

So, why did the Fed decide to loosen monetary policy, in spite of, the favorable economic outlook? One reason is inflation. The Fed’s preferred inflation gauge, the deflator of personal consumption expenditures, runs well below the Fed’s 2 % inflation target, currently at 1.4 % (June). The same holds for consumer price (CPI) inflation which is only marginally higher at 1.6 % (June). More importantly, though, is the inflation outlook, which is, predominantly, driven by expectations about future price developments as well as the expected state of the economy. Measures of inflation expectations can be derived from financial markets (market-based) as well as surveys (survey-based). Market-based inflation expectations tend to be more volatile than survey-based measures, as they carry a time-varying risk premium component. In the United States, survey-based inflation expectations remain well-anchored at the Fed’s inflation target (Figure 3). Market-based inflation expectations are currently below the inflation target, though, can move back to 2 % very quickly as happened in July. The FOMC members expect inflation to converge to the 2 % target by 2021, also being facilitated by a lower federal funds rate.

Besides promoting a faster return to the inflation target, President Powell justified the decrease in the federal funds rate as an insurance “against downside risks from weak global growth and trade policy uncertainties”. It was further emphasized that the rate cut should not be interpreted as the start of an extensive cutting cycle but rather as a mid-cycle adjustment to prolong the economic expansion. Previous mid-cycle adjustments consisted of three rate cuts. The federal funds rate was lowered from 6 % to 5.25 % in 1995/96 and again from 5.5 to 4.75 % in 1998. Financial market expectations of the future path of the federal funds rate imply two more rate cuts in 2019 and one-to-two cuts in 2020 (Figure 4). Thus, markets currently expect a more aggressive monetary easing than past mid-cycle adjustments would imply. As previously the FOMC statement emphasized that the future path of the federal funds rate will be data-dependent. At the press conference, Powell emphasized the importance of trade tensions and the limited experience central bankers’ have regarding their broader macroeconomic implications. “It’s learning-by-doing”, so Powell.

The US economy is healthy and well-balanced. Yet, global factors, predominantly trade policy disruptions, put downside risks to the outlook. Uncertainty undermines business confidence, whose effects on output the Fed finds difficult to assess. The ISM manufacturing Purchasing Manager Index (PMI), a leading business sentiment indicator, has dropped to its lowest level since August 2016 (51.2 in July). In light of deteriorating global trade, demand is weak in the manufacturing sector and so is business investment. The Fed’s insurance cut was, therefore, predominantly driven by uncertainties regarding the global outlook rather than the current state of the US economy.

Whether the Fed’s mid-cycle adjustment to a somewhat more accommodative stance of monetary policy was necessary, remains ambiguous. It is definitely not a clear-cut case for monetary policy intervention. Two members of the FOMC (Esther George and Eric Rosengren) would have preferred to keep the federal funds rate constant. The Fed has delivered, at least partly, to the frontrunning of financial markets and President Trump’s wish for lower interest rates.

Authors

Martin Ertl Franz Xaver Zobl

Chief Economist Economist

UNIQA Capital Markets GmbH UNIQA Capital Markets GmbH

SportWoche ÖTV-Spitzentennis Podcast: ÖTV-Damen dominieren beim WTA-125-Challenger in Kitzbühel, 3x Karrierehoch in Woche 29

Bildnachweis

1.

GDP growth by main expenditure components

2.

US Labor Market (non-farm payrolls)

3.

Inflation & Inflation Expectations

4.

Federal Funds Rate Market Expectations

5.

Interest Rates

Aktien auf dem Radar:Frequentis, Zumtobel, AT&S, Austriacard Holdings AG, Polytec Group, Rosenbauer, Verbund, OMV, voestalpine, Porr, Fabasoft, Heid AG, Reploid Group AG, Marinomed Biotech, Wolftank-Adisa, Wiener Privatbank, BKS Bank Stamm, Wolford, Amag, Bawag, EuroTeleSites AG, CPI Europe AG, Österreichische Post, Telekom Austria, UBM.

Random Partner

Erste Group

Gegründet 1819 als die „Erste österreichische Spar-Casse“, ging die Erste Group 1997 mit der Strategie, ihr Retailgeschäft in die Wachstumsmärkte Zentral- und Osteuropas (CEE) auszuweiten, an die Wiener Börse. Durch zahlreiche Übernahmen und organisches Wachstum hat sich die Erste Group zu einem der größten Finanzdienstleister im östlichen Teil der EU entwickelt.

>> Besuchen Sie 55 weitere Partner auf boerse-social.com/partner

Latest Blogs

» Österreich-Depots: Wollen den Weg zum 2. Mal mit Marinomed gehen (Depot ...

» Börsegeschiche 20.7.: BA-CA, Libro, Agrana, Amag (Börse Geschichte) (Bör...

» Nachlese: WTA Kitzbühel, Lucia Mayr-Harting (audio cd.at)

» PIR-News zu Andritz, Frequentis, Erste Group, Addiko, cyan (Christine Pe...

» Unser Song ist Top100 und das 76-seitige Zertifikate Magazine 20 Jahre Z...

» Wiener Börse Party #1202: ATX unverändert, der IPO-Index trudelt und ist...

» Wiener Börse zu Mittag unverändert: Frequentis, Palfinger und Semperit g...

» Börse/Sport-Inputs auf Spotify zu u.a. Sinja Kraus, Julia Grabher

» ATX-Trends: Frequentis, AT&S, RBI, Addiko, Marinomed ...

» LinkedIn-NL: Yeah, unser Song ist Top100! Und die grosse Zertifikate Son...

Useletter

Die Useletter "Morning Xpresso" und "Evening Xtrakt" heben sich deutlich von den gängigen Newslettern ab.

Beispiele ansehen bzw. kostenfrei anmelden. Wichtige Börse-Infos garantiert.

Newsletter abonnieren

Runplugged

Infos über neue Financial Literacy Audio Files für die Runplugged App

(kostenfrei downloaden über http://runplugged.com/spreadit)

per Newsletter erhalten

- Wiener Börse: ATX geht fester aus der Montag-Sitzung

- Wiener Börse Nebenwerte-Blick: Marinomed steigt f...

- Wie Marinomed Biotech, Wolftank-Adisa, Heid AG, F...

- Wie Wienerberger, Verbund, OMV, Bawag, Lenzing un...

- Österreich-Depots: Wollen den Weg zum 2. Mal mit ...

- Börsegeschiche 20.7.: BA-CA, Libro, Agrana, Amag ...

Featured Partner Video

Kapitalmarkt-stimme.at daily voice: Servus Peter Brezinschek! Reden wir doch kurz über Andritz, AT&S, den Standort sowie Sport...

kapitalmarkt-stimme.at daily voice auf audio-cd.at. Im Zusammenhang mit einem aktuellen Projekt hat mich am Mittwoch Peter Brezinschek besucht. Und da haben wir natürlich gleich was aufgenommen, gu...

Books josefchladek.com

Atlantic

2025

form.

Asylum

1987

Koks Forlag & Preus Fotomuseum

Kobe 1995 After the Earthquake

1995

Telescope

Ci-contre

2004

Ann und Jürgen Wilde

Ralph Gibson

Ralph Gibson